Non-standard applications are predictable in the Richmond metro. They show up in Richmond City when an applicant is new to the area, changing roommates, or starting a job next week. They show up in Henrico County when applicants have variable pay structures, remote work income, or thin credit files. They show up in Chesterfield County and Hanover County when applicant volume is lower and pressure rises to approve the “best available” file before the next showing cycle.

The risk is not that documents look different. The risk is what happens when the screening standard quietly changes in response. That is where disputes tend to originate, because the file stops being comparable and the decision stops being reconstructable.

A defensible approach treats non-standard files as a process problem under pressure. Screening stays stable when screening rules that stay consistent remain fixed, and acceptable proof pathways are predefined. The record holds up when verification notes that hold up capture what was verified, what could not be verified, and why the application did or did not satisfy the same standard applied to every other applicant.

Table Of Contents

Why non-standard screening increases risk

What “non-standard” means in practice

Where good files break under pressure

Income verification when pay stubs do not exist

Thin credit files and “no hit” reports

Rental history gaps and hard-to-verify references

Identity verification and document integrity

Fraud risk under time pressure

Consistency, Fair Housing, and alternative pathways

Defensible exception handling

Two scenarios: common and messy

Cost drivers and time drivers

Common mistakes that create disputes

Simple decision path

FAQ

Conclusion

Next Step

Key Takeaways

Non-standard files are safest when approval criteria do not change, and only the acceptable proof combinations change.

Undocumented substitutions are the fastest way to create later disputes, because comparability and reasoning cannot be shown.

Virginia caps application fees and security deposits, so “solve it with money” has hard legal limits.

If a consumer report influences a denial or less favorable terms, adverse action notice obligations follow.

Consistency is a Fair Housing control, because the highest-risk pattern is offering different options to similarly situated applicants.

Why Non-Standard Screening Increases Risk

Screening works when it is repeatable. Risk rises when a file falls outside the default template and the only tool left is judgment.

Non-standard files create predictable pressure points:

Verification channels are slower than the leasing timeline.

Documents are easier to misread because they are unfamiliar or incomplete.

Decision-makers substitute plausibility for corroboration.

Exceptions multiply, and the file becomes hard to defend later.

The downstream cost is rarely immediate. The cost shows up later as delinquency, enforcement hesitation, or a dispute where the only question that matters is what can be proven.

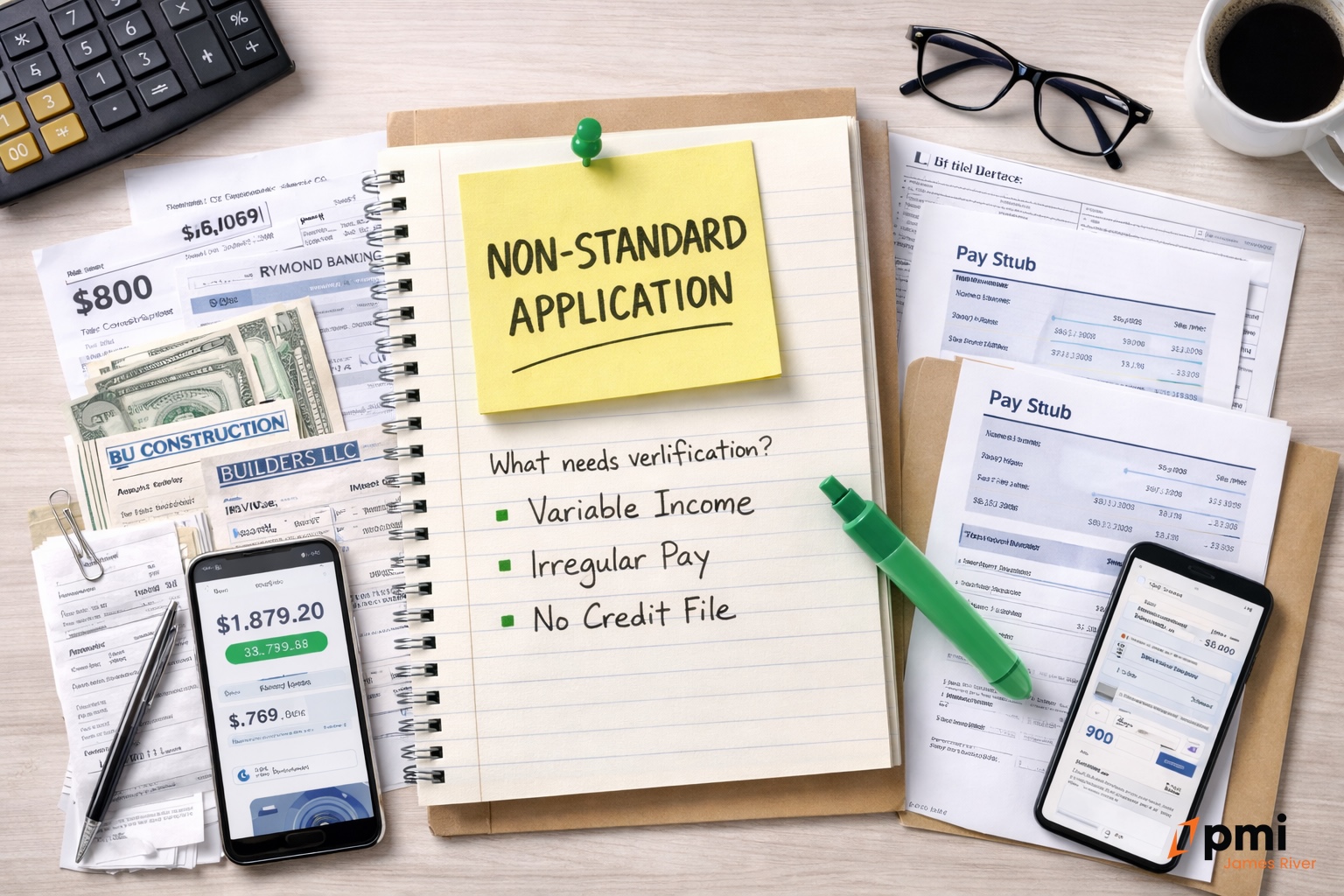

What “Non-Standard” Means In Practice

Non-standard does not mean “high risk” by default. It means the application cannot satisfy the default proof package in the default way.

Common patterns. These show up across the Richmond metro and are usually about documentation format, timing, or continuity.

Variable income. Commission, contract work, seasonal hours, overtime-heavy roles, or fluctuating schedules.

Self-employed income. Business owners and contractors whose pay is not a payroll stub.

New job, no deposits yet. Offer letter exists, payroll deposits do not.

Thin credit file. Limited history, recent rebuild, or “no hit” outcomes.

Non-traditional housing history. First-time renters, roommate transitions, or long periods living with family.

Split payor structures. A third party pays part or all of the rent, or the resident portion is smaller than the gross rent.

A stable policy treats these as known patterns with defined proof pathways, not as one-off exceptions.

Where Good Files Break Under Pressure

Most screening failures are not “no verification.” They are partial substitutions that never get reconciled.

Substitution drift. A document is accepted “for now,” with the intention to verify later. Approval momentum tends to make “later” disappear.

Comparability collapse. Different applicants are offered different alternatives with no written rule, and the file becomes hard to defend even if the decision felt reasonable.

Documentation gaps. Notes focus on impressions instead of facts. Months later, the facts are what matter.

The fix is not harsher screening. The fix is a clear proof menu that satisfies the same eligibility criteria, paired with short, factual notes created at the time of the decision.

Income Verification When Pay Stubs Do Not Exist

Income verification is where non-standard screening most often turns into future nonpayment. The failure mode is treating any money document as proof without showing continuity.

A defensible approach relies on one rule.

Corroboration rule. Income is verified when at least two independent indicators agree, and the agreement supports continuity rather than a single good month.

That rule can be satisfied through different document combinations.

Self-employed income. A strong file usually ties deposits to the activity that generated them.

Deposit history that shows recurring inflows, plus

Documents that explain what the inflows represent (invoices, contracts, platform statements), plus

A short note describing the lookback window and why inflows are expected to continue.

Variable wage income. A strong file avoids treating the most recent stub as representative.

Pay documentation that shows the pay structure, plus

Deposit history across a longer window to show the pattern, plus

A short note describing variability and how the pattern supports the rent obligation.

New job with an offer letter. A strong file treats an offer letter as one indicator, not the indicator.

Offer letter, plus

Independent employer confirmation of start date and compensation, plus

Verified accessible funds sufficient to bridge the pre-payroll gap.

Virginia’s caps matter here because they limit the “charge more” and “collect more” shortcuts.

Application fees are capped at $50, exclusive of actual out-of-pocket third-party screening costs, with a lower cap for certain HUD-regulated units.

Security deposits may not exceed two months’ periodic rent.

Those constraints are why continuity logic and corroboration do more risk control work than ad hoc financial demands.

Thin Credit Files And “No Hit” Reports

A thin credit file is missing data, not automatically negative data. Treating “no score” as “fail” can push decisions into a blunt rule that denies otherwise qualified applicants who simply lack report depth.

A defensible approach separates three questions.

- What is known. Confirmed items that can be relied on, such as verified tradelines, verified collections, or verified eviction records where lawfully permitted and applied consistently.

- What is unknown. No file, limited file, or a report too new to reflect current stability.

- What substitutes exist. Corroborated income continuity, verified deposit patterns, verified housing performance where possible, or a defined guarantor pathway.

Consumer reporting obligations often appear here because “thin file” cases frequently lead to conditional approvals. The CFPB describes adverse action notice requirements and the applicant’s rights, including the right to a free copy of the report within 60 days and the right to dispute inaccurate information. The FTC similarly emphasizes the 60-day free copy right in the tenant background check context.

Rental History Gaps And Hard-To-Verify References

Rental history gaps are common and not automatically disqualifying. The risk is pretending the gap is neutral when verification is weak.

A practical approach evaluates housing history in tiers.

- Verified housing performance. Independently confirmed contact information, specific payment and conduct facts, clear dates and addresses.

- Partially verified history. Some confirmable elements, with documented gaps.

- Unverified references. Information provided, but verification cannot be independently confirmed.

Unverified does not always require denial. It does require that the decision lean more heavily on other corroboration categories, and that notes clearly state what was not verifiable and how the application met the standard anyway.

Identity Verification And Document Integrity

Identity verification should happen before qualification momentum builds. Non-standard files increase integrity risk because unfamiliar formats are easier to misread and time pressure makes shortcuts feel reasonable.

Identity checks that tend to hold up are simple and consistent.

- Cross-document consistency. Names, dates, and addresses align without unexplained variation.

- Source-document preference. Source documents are favored over screenshots. A screenshot can support context, but it should not be treated as primary verification.

- Minimum necessary data. Collect what is needed to establish identity and eligibility, then stop. Over-collection increases privacy risk without improving the decision.

Fraud Risk Under Time Pressure

Fraud is not required for non-standard screening to fail, but fraud thrives under the same conditions that cause verification breakdowns: urgency, improvisation, and unlogged exceptions.

Time pressure shows up in predictable forms:

Same-day approval expectations tied to a move-in date.

Requests to “hold” a unit based on partial proof.

Commitments to verify after keys are exchanged.

A defensible policy treats time pressure as a risk trigger, not as permission to relax standards. The safest response is a proof menu that can be satisfied quickly without turning into discretionary judgment.

Consistency, Fair Housing, And Alternative Pathways

Fair Housing risk is not created by alternative documentation. Risk is created by who is offered alternatives and how consistently they are offered.

Virginia’s Fair Housing Office guidance explicitly warns that standards set too high may be viewed as attempting to keep certain groups out of rentals, and it emphasizes that screening should focus on ability to pay and be set as a standard. Separately, HUD has issued guidance addressing fair, transparent, and nondiscriminatory tenant screening policies, including issues created by third-party screening tools.

A defensible system has four characteristics.

- Predefined alternatives. Alternate proof pathways are written in advance.

- Comparable options. Similarly situated applicants are offered the same pathways.

- Documented acceptance or rejection. Notes state which pathway was used and why it satisfied the standard, or why it did not.

- Stable eligibility criteria. The underlying approval requirements do not shift based on urgency, persuasion, or comfort with the file format.

Defensible Exception Handling

Exception handling does not mean “make it work.” It means controlling variability without letting the standard drift.

Exception handling holds up when:

The pathway is predefined as an allowed proof combination.

The eligibility standard remains fixed and objective.

The reasoning is documented contemporaneously in short, factual notes.

The file can be reconstructed months later without relying on memory.

This becomes especially important when tenant screening reports are used. The report can provide data, but the housing provider still owns the decision logic and must be able to show that the same logic was applied across files.

Two Scenarios: Common And Messy

Scenario 1: Domestic Self-Employed Applicant In Henrico County

The applicant is a contractor with no pay stubs, uneven monthly income, and a credit file that does not reflect current cash flow. The applicant provides bank statements and invoices.

A defensible file focuses on corroboration and continuity.

- Corroboration. Deposits show recurring inflows that plausibly match the invoices.

- Continuity note. Notes state the lookback window, describe variability, and explain why the recurring inflows support the rent obligation across the lease term rather than in a single strong month.

- Consistency. The same proof menu is available to any self-employed applicant, regardless of job type.

If a consumer report contributed to a conditional term, the adverse action analysis stays relevant. The CFPB identifies conditional outcomes like requiring a co-signer or a larger deposit as adverse action examples when driven by report information.

Scenario 2: New Job In Richmond City, Thin Credit, And A Housing History Gap

The applicant has an offer letter for a role starting in two weeks, limited report depth, and no recent landlord reference because they were living with family.

This is where weak processes often collapse into “it feels fine,” and the file later becomes hard to defend.

A defensible approach addresses three constraints.

- Employment verification. The start date and compensation are independently confirmed.

- Bridge funds logic. Funds are verified as accessible and sufficient to cover the pre-payroll gap, and notes plainly describe why the bridge period is covered.

- Housing history treatment. The gap is documented as a gap, not converted into an unverifiable positive reference.

Cost Drivers And Time Drivers

Non-standard screening becomes expensive when proof pathways are undefined.

Time drivers. Employer confirmations, document collection delays, and reference checks are common bottlenecks. When the proof menu is predefined, the bottleneck becomes selecting the right pathway rather than inventing a pathway.

Cost drivers. Paid third-party checks add cost, and Virginia’s application fee structure limits how that cost can be handled because the fee cap is fixed and only actual out-of-pocket third-party screening costs can be charged beyond the cap. Deposit caps also limit the ability to offset verification risk with larger refundable deposits.

The highest-leverage investment is usually not more documents. It is clearer pathways and better notes.

Common Mistakes That Create Disputes

Neatness bias. A clean PDF and a confident narrative are not verification.

Balance equals income thinking. A balance can reduce immediate risk but does not prove continuity.

Unlogged substitutions. Substitutions without notes become impossible to defend later.

Inconsistent alternative options. Offering one applicant a guarantor path while denying another similarly situated applicant the same path, without a written distinction, is where comparability fails.

Adverse action gaps. When report information influences an unfavorable decision or less favorable terms, notices and disclosures protect both the applicant’s rights and the defensibility of the process.

Simple Decision Path

Start with written eligibility criteria that remain fixed across properties and across the Richmond metro.

Define proof menus for common non-standard patterns as acceptable document combinations that satisfy the same eligibility criteria.

Apply objective triggers for deeper verification based on inconsistencies or missing corroboration, not impressions.

Document the pathway used, what was verified, what could not be verified, and why the application did or did not satisfy the standard.

When a consumer report influenced denial or less favorable terms, treat adverse action documentation as part of compliance discipline.

FAQ

What counts as non-standard documentation in rental screening?

Non-standard documentation is any file that cannot satisfy the default proof package in the default way, such as self-employment, variable income, new jobs without deposits yet, thin credit files, or limited verifiable housing history.

Does non-standard screening require lower standards to approve good applicants?

No. A defensible approach keeps the approval criteria fixed and provides predefined proof combinations that can satisfy the same criteria.

Are bank statements acceptable substitutes for pay stubs?

They can reduce risk when they are part of corroboration and continuity logic, not when they are treated as standalone proof with no explanation of what deposits represent and why they are expected to continue.

What does Virginia law allow for application fees?

Virginia caps application fees at $50, exclusive of actual out-of-pocket third-party screening costs, with a lower cap for certain HUD-regulated units.

Can a higher security deposit substitute for weak verification in Virginia?

Virginia does not allow security deposits above two months’ periodic rent, which limits the ability to offset verification risk by collecting more refundable money.

When do adverse action notices apply in tenant screening?

When a consumer report influences a denial or less favorable terms. The CFPB describes required elements, including the reporting company’s contact information, the right to a free copy within 60 days, and the right to dispute inaccuracies.

Conclusion

Non-standard screening is not primarily a document problem. It is a consistency problem. When a process depends on improvisation, verification becomes discretionary at the moment it matters most, and the file becomes difficult to defend later.

A stable system treats non-standard files as predictable patterns with predefined proof menus, objective triggers for deeper verification, and contemporaneous notes that preserve comparability. Virginia’s statutory caps on fees and deposits reinforce the same reality: process discipline replaces ad hoc financial demands.

Next Step

Screening outcomes stay steadier when screening rules that stay consistent are written as fixed criteria paired with proof menus, not case-by-case exceptions. Files also hold up longer when verification notes that hold up preserve the corroboration logic and clearly label what was unverified at the time of the decision.